Introduction

Blockchain technology, often associated with cryptocurrencies, has significantly impacted numerous industries due to its decentralized, secure, and transparent nature. This innovative technology has revolutionized the way data is stored and shared, providing a secure and tamper-proof system that enhances trust among users.

What is Blockchain?

Unlike traditional centralized databases administered by a single company, blockchain is based on an end-to-end network in which each node has a copy of all the accounts recorded, especially the money it has spent and received. This decentralized structure improves the security, transparency, and resilience of the data.

How does Blockchain Work?

Blockchain generates a series of blocks that are linked together:

Genesis Blocks: When dealing with Bitcoin, cryptocurrency itself creates the first block. There is no data associated with this block. It has a hash value, and the previous hash value was all zeroes. The hash is inputted into the block header and encrypted alongside other block information, forming a chain of interconnected blocks.

Block 1: The next block of the blockchain will contain some data, potentially transactional information.

Block 2: This block will also include data from previous transactions. The previous hash value will be used as the hash for Block 1. This is why we’ve been considering references as cryptographic hashes.

Block 3: The same applies to block 3 as well. Every block contains two hashes: the hash of the previous node and the hash value of the current block. These hash values will serve as references for earlier blocks.

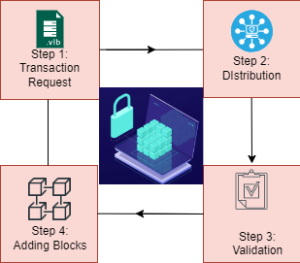

Transaction Process: Depending on the blockchain being used, transactions follow a specific protocol. For example, when you initiate a transaction on Bitcoin’s blockchain using your cryptocurrency wallet, the app that acts as the interface for the blockchain triggers a sequence of events as an illustration.

In Bitcoin, your transaction is sent to a memory pool, where it is kept and queued until a miner or validator selects it. After being entered into a block and filled with transactions, the block is closed and encrypted using an encryption mechanism.

Blockchain Applications and Use Cases

It is now understood that transactional data is stored in blocks on the Bitcoin blockchain. Today, a blockchain powers over 23,000 additional cryptocurrency systems. However, Blockchain turns out to be a dependable method for preserving information about various kinds of transactions.

Supply Chain

Similar to the IBM Food Trust case study, suppliers have the ability to utilize blockchain technology to document the sources of the materials they procure. This would enable businesses to confirm the legitimacy of not only their goods but also popular labels like “Local,” “Organic,” and “Fair Trade.” According to Forbes, the food sector is using blockchain technology more and more to monitor the safety and route of food as it travels from farm to consumer.

Banking and Finance

Financial institutions operate only during business hours, typically five days a week. This implies that you will probably have to wait until Monday morning for the money to appear in your account if you attempt to deposit a check on Friday at 6 PM. Because of the enormous amount of transactions that banks must process, it may take one to three days for your deposit to be verified, even if you make it during business hours. Blockchain, however, is constantly active. No matter the time of day or week or the holidays, customers may be able to see their transactions processed in a matter of minutes or seconds if banks integrate blockchain technology. Banks can also use blockchain to facilitate safer and faster money transfers across institutions. Because of the scale of the amounts involved, banks may incur considerable expenses and hazards during the brief time the money is in transit.

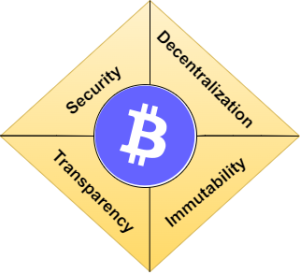

Features of Blockchain

- Decentralisation: Uses an end-to-end network with no central authority

- Immutability: Once captured, data cannot be modified or deleted

- Transparency: All network users can access the public ledger

- Security: Data is protected by sophisticated encryption algorithms

Advantages of Blockchain

- Security: High levels of cryptographic security safeguard data from unauthorized access and manipulation

- Transparency: Each transaction is accessible to all participants, which increases confidence and responsibility

- Efficiency: Reduces the need for intermediaries, resulting in faster transactions and lower costs

- Traceability: Each transaction leaves a clear and verifiable audit trail

Conclusion

Blockchain technology represents a fundamental shift in how we see decentralization, transparency, and data security. It has the potential to drastically improve and disrupt a wide range of industries while addressing some of the most pressing issues with data management and transaction integrity. Blockchain technology’s applications are projected to expand as it develops and matures, driving innovation and encouraging a more transparent and secure digital world.